As per the Indian income tax laws, every earning citizen of India is required to pay an income tax to the Government as per the applicable income tax rate. To ensure hassle-free income tax payment by citizens, the Income Tax Act of 1961 mandates every person or company to deduct tax at source while making salary or fee payments above a certain threshold.

What is TDS?

The TDS full form is tax deducted at source. As per the concept of TDS, a person, or a company (known as the deductor) who is liable to pay a salary or fee to another person (known as the deductee) can deduct a TDS amount before making the payment. The TDS can be deducted only at a specified rate as prescribed by the income tax department.

After deducting the TDS amount, the deductor has to submit it to the Central Government and also issue a TDS certificate to the deductee.

What is a TDS certificate?

A TDS certificate is a document that validates TDS deduction. A deductee can use this document to claim the tax credit and get a tax refund from the Government (if any). The TDS certificate is issued to a deductee by a deductor. TDS certificates are issued as Form 16 and Form 16A.

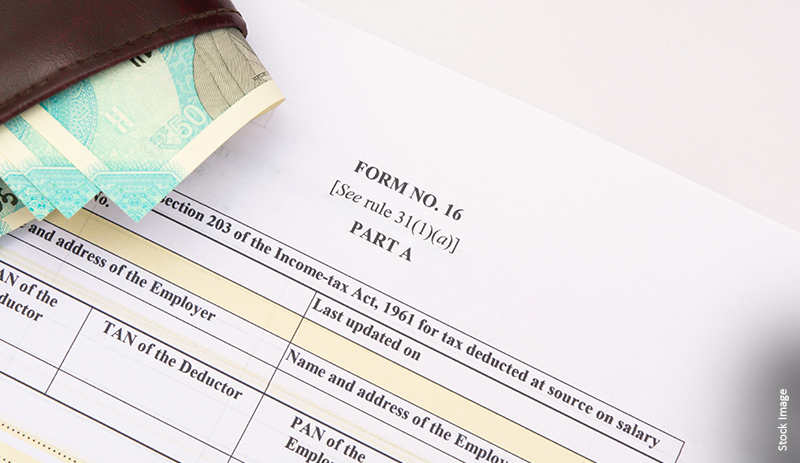

What is Form 16?

Form 16 is the TDS certificate issued for TDS deducted from salary payments. Hence, these TDS certificates are issued by employers to their employees. In simpler words, Form 16 acknowledges that a certain TDS amount has been deducted from an employee’s salary and has been submitted to the Government by their employer.

Since Form 16 is issued after the end of every fiscal year, it is also known as an annual TDS certificate. Form 16 consists of two parts – Part A and Part B.

- Part A contains all information about the employer and employee, including their names, PAN and TAN details, addresses, period of employment, etc.

- Part B contains the details of the salary paid to the employee, payable income tax amount, TDS deduction details, other applicable income tax deductions, etc.

As per Section 192 of the Income Tax Act, all employers are required to deduct a 10% TDS from the salary payments of their employees if the annual salary amount exceeds Rs. 2.5 lakh.

What are the due dates for issuing Form 16?

Form 16 must be issued to the employers by June 15 after the end of the financial year for which it is being issued. For example, if an employer is issuing Form 16 for TDS deductions during the year 2022-23, he or she must issue the TDS certificates to his or her employees by June 15, 2023.

What is Form 16A?

Form 16A is also a TDS certificate, but it is issued for TDS deductions on payments other than salaries. These can include interest payments, brokerages, incentives, rent payments, lottery prizes, etc. Form 16A can be issued by anyone who is making a payment to another person or a company above a specified limit.

Below are the common TDS deductions made from non-salary payments as specified under Sections 193 and 194 of the Income Tax Act:

- 10% TDS is deducted from interest earned on securities.

- 30% TDS is deducted from winnings from lotteries, crossword puzzles, card games, horse races, etc.

- 5% TDS is deducted from insurance commissions.

- 20% TDS is deducted on the repurchase of mutual fund units.

- 10% TDS is deducted from rent payments.

Like Form 16, Form 16A also contains the name and address of the deductor as well as the deductee, their PAN and TAN details, the date on which the payment (for which the TDS has been deducted) was made, the amount, and nature of the payment. Form 16A is issued at the end of every quarter and hence, is also known as a quarterly TDS certificate.

How to get Form 16 and Form 16A?

One can ask the deductor to provide duly filled Form 16 or Form 16A. These forms can also be downloaded by visiting the official website of the Income Tax Department. After downloading the applicable TDS certificate, one can ask the deductor to fill in the details and provide the authorized signatory.

The final words

TDS certificates are issued as Form 16 or Form 16A by the deductor. They act as proof that the TDS amount has been deducted from the payment made to the deductee and is submitted to the Government. In case a deductor fails to issue a TDS certificate before the due date, he or she may have to pay a penalty of ₹100 per day for each certificate.

Disclaimer- This article is based on the information publicly available for general use as well as reference links mentioned herein. We do not claim any responsibility regarding the genuineness of the same. The information provided herein does not, and is not intended to, constitute legal advice; instead, it is for general informational purposes only. We expressly disclaim any liability, which may arise due to any decision taken by any person/s basis the article hereof. Readers should obtain separate advice with respect to any particular information provided herein.

Table of Contents

Table of Contents